|||

|||

Despite huge amounts of publicity and government efforts to tackle the the gender pay gap, it remains a serious issue. It affects women in most industries: from artists and academics to journalists and doctors.

We’ve researched some of the particular problems facing the UK’s finance industry when it comes to the gender pay gap. Across finance as a whole, women earn 27.2% less than men an hour, on average. When it comes to bonuses the gap is nearly 50%. Our research shows how this plays out at different levels of the finance industry.

Progress on gender pay issues in this sector has been too slow, fragmented and uneven over the past ten years. The UK government introduced legislation requiring employers with more than 250 employees to report annually their gender pay gap publicly beginning April 2018. The principle is that greater transparency will reduce the gender pay gap, but the evidence so far suggests this is not enough.

The gender pay gap is a global phenomenon. At Davos, IMF chief, Christine Lagarde raised the gender imbalance in the financial sector, saying: “The numbers are just appalling … you have 20% of board members in the financial sector who are women, and you only have 2% of CEOs who are women.” This, despite the fact that it is “business common sense … that diversity actually precipitates productivity and is good for all”.

Our findings

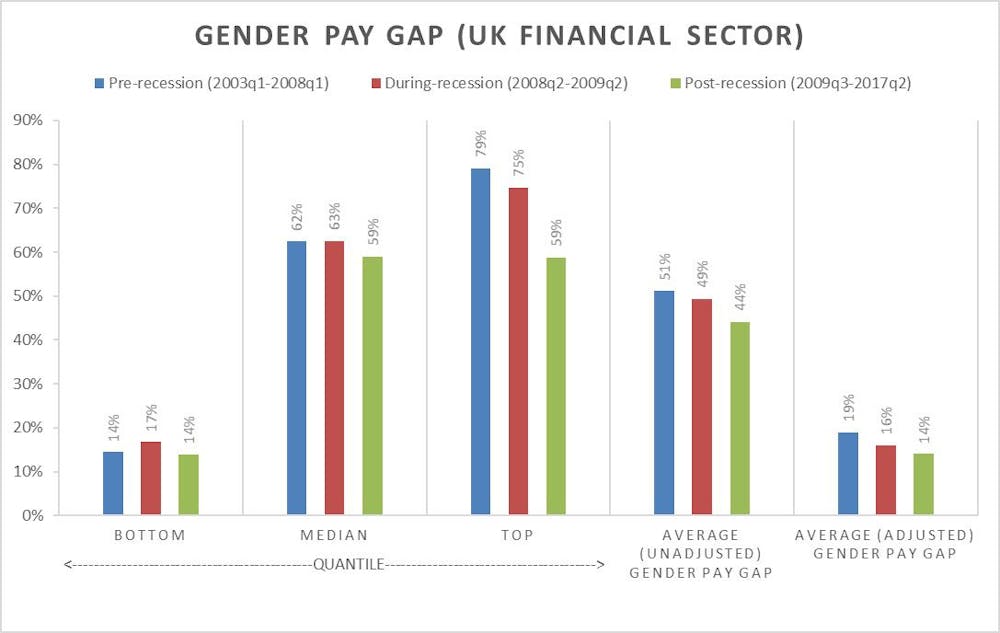

The financial services industry was called out in the UK government inquiries that followed the 2008-09 financial crisis for receiving £1.3 trillion of taxpayer support and for unsafe pay policies (including bonus culture), which contributed to the recession. At the same time, the government’s Equality and Human Rights Commission exposed the particularly large gender pay gap in the sector, long working hours, inflexible work and a male-biased culture.

We began our research expecting that this kind of exposure and public dislike of the sector might well have led responsible organisations to radically review their culture and pay systems. Yet, we were aware that the state initiatives only put voluntary pressure on financial services to reform their pay and culture, so we might see little change.

Indeed, overall, we found there to be only a marginal decline in the pay gap since the recession – rather than a radical change. Our study exposed differences between groups, with the gender pay gap substantially higher among the financial industry’s highest earners. Between 2009 and 2017 the gap ranged from 13.8% among the lowest earners (that is, at the 10th quantile) compared to 58.6% among the highest earners (90th quantile), resulting in the irony that the more successful the woman, the greater the pay gap between her and her male counterpart.

So Lagarde is right to call for more diversity in the financial services sector, but it is not enough to simply promote women and then pay them less than men in the same positions.

We were not only concerned with exposing inequality at the highest levels but across the spectrum of roles and wages. At the lower levels of pay, while the pay gap was less, there was no improvement over the period we looked at.

Our paper also identified contradictory patterns. Despite the decline in trade union membership in recent decades, trade unions still had a positive effect – union membership and collective bargaining led to a reduction in the gender pay gap.

But, particularly concerning is that ethnicity was related to a higher pay gap and the study also uncovered a post-recession increase in working hours, which contributes to an increase in the pay gap as women often bear the brunt of caring responsibilities. As an earlier survey and evidence to the Treasury’s Women in the City report on increased working hours by the union Unite also found, long working hours and “presenteeism” are part of a male culture in which women may be excluded as not “fitting in” or exclude themselves as this way of working is disproportionately time greedy.

Window dressing?

It is clear that financial firms are investing in diversity strategies. But it is hard not to wonder how much of the investment is window dressing, or else just poorly implemented. A striking example is Lloyds Banking group’s Inclusion and Diversity Strategy. Lloyds’ strategy to improve the pay gap is to increase the proportion of women in senior roles so that “the gender gaps will reduce over time”. This strategy and their wider diversity initiatives have received external recognition, and the bank has received numerous accolades.

But, despite their prize-winning diversity initiatives, Lloyds’ Banking Group reported an average pay gap figure of 31.5% in 2018 (the average for the sector is 27.2%) and its bonus gap was more than 60% (the average is just under 50%).

The sector as a whole continues to be steeped in discriminatory practices with respect to pay and unequal treatment favouring men and disincentivising women through the persistence of its alpha-male culture and associated long hours. Financial services has undoubtedly introduced and promoted positive diversity initiatives, but these have been undermined by things like discretionary bonuses and increasingly long working hours.

Plus, it is clear that gender equality is still not a strategic priority with the effect that the second round of reporting due in April 2019 is already indicating a worsened pay gap for four in ten firms. Change is unlikely without external pressure, whether from unions, women’s networks and pressure groups. But ultimately the state must introduce more financial sanctions on those organisations that show no progress in closing the gender pay gap.![]()

Geraldine Healy is professor of employment relations at Queen Mary University of London and Mostak Ahamed is lecturer in finance at the University of Sussex. This article is republished from The Conversation under a Creative Commons license. Read the original article.

Despite gender pay gap reporting, there has been little progress towards closing the gap, particularly in financial services. Are fines the answer?